Comprehensive list of MAGI for IRMAA

Medicare’s Income Related Monthly Adjustment Amount (IRMAA) is quickly becoming a problem for retirees and by government projections it will not slow down in the near future too.

Between 2023 to 2031 the federal government is projecting that over 13 million retirees will pay over $354 billion in surcharge/taxes through IRMAA while on Medicare.

IRMAA is simply a tax on specific income you generate while you’re in the Medicare program.

The more income you have, the higher your Medicare Part B and Part D premiums will be and the higher your Medicare Part B and D premiums are the lower Social Security benefit you will receive.

IRMAA simply provides revenue for the Medicare program while it also lowers the obligation Social Security must pay out to retirees.

It is a win – win for the government.

What is income for IRMAA?

The Social Security Administration (SSA) defines income for as being:

AGI (adjusted gross income) plus any tax-exempt interest you may have for the year or

Everything on lines 2a and 11 of the 2022 IRS tax form 1040.

What really counts as income for IRMAA:

Not all sources of income will apply to you and many some sources of income have the ability to implement a deduction too.

- Wages

- Taxable Social Security benefits.

- Up to 85% of your Social Security can be taxable.

- Capital Gains.

- From any nonqualified investment.

- Sale of primary residency does have a deduction up to certain limits.

- Tips.

- Dividends.

- Interest (from):

- Municipal Bonds.

- Savings Bonds.

- Treasury Bills, Notes and Bonds.

- Savings Bonds.

- Bank accounts (savings and checking).

- Money Markets.

- Certificates of Deposits (CD’s).

- Corporate Bonds.

- Deposited Insurance Dividends.

- Any other interest if the total is above $600.00 for the year.

- Income from

- Taxable portion from Pensions.

- Incarceration (yes, any money you earn if you are in jail counts too.).

- Taxable portions from any Trusts.

- Taxable portions from ABLE Accounts..

- Distributions from Tax-Deferred Investments which include:

- Traditional IRA

- Traditional 401(k)

- Traditional 403(b)

- Keough Accounts

- SEP IRA’s

- 457 accounts

- Annuities.

- Other

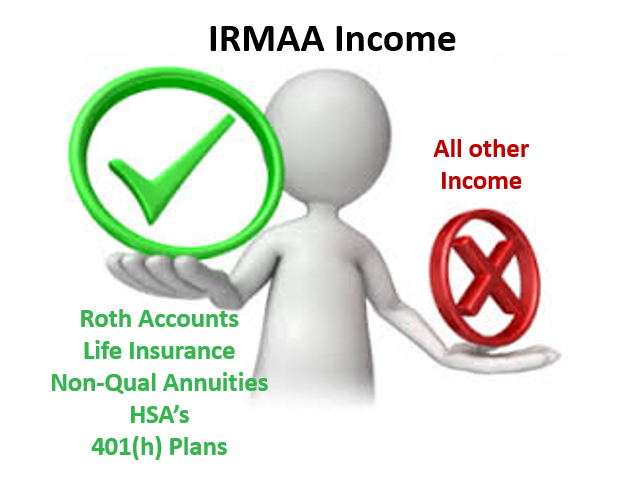

What does NOT count towards IRMAA that you can use for income?

Unfortunately, this list is exponentially much shorter than what the SSA will use against you:

- Distribution from Roth Accounts.

- Cash Value from Life Insurance.

- Tax-excludable income from nonqualified Annuities.

- Qualified distributions from Health Savings Accounts (HSA’s).

- Qualified distributions from 401(h) Plans.

- Qualified loans from your primary residency (think Reverse Mortgage).

What may counts as MAGI for IRMAA:

Disability payments.

A recent article from Forbes delves into if payments you are receiving from an a disability claim will count as MAGI or income and it all comes down to who owns the policy.

If the your employer owns the disability policy and the premiums were paid by that employer than the disability payments are taxable and count as MAGI for IRMAA.

BUT, if you own the policy and you pay the premiums with after-tax dollars then any payment you receive is tax free.

Is IRMAA That big of deal?

IRMAA is a tax and historically no tax the federal government creates either goes away or ever gets smaller, and IRMAA will be no different especially if you look at what the federal government is saying.

According to the federal government when it comes to IRMAA:

The IRMAA surcharges (taxes) will grow by at least 6.00% annually for the next 8 years and will continue at an inflation rate close to 5% after that.

What starts out being only a couple of thousands of dollars will grow to more than a few thousand dollars over the next 8 years and then before you know it will be more than couple tens of thousands of dollars.

The number of retirees reaching IRMAA will double over the same time frame as the Trustees are expecting that roughly 13.5 million Medicare beneficiaries will reach IRMAA by 2031.

IRMAA will generate over $354 billion is surcharges over the next 8 years.

IRMAA is not going to get smaller, nor will it even go away.