Social Security Going Broke…Not Really

When it comes to the Social Security program there seems to be a consistent alarm going off from the government and the media that the program is going broke and will be bust sooner rather than later.

The data that is provided backs this statement up, as well as, a plethora of financial experts who are continuously chanting the same mantra, but when you dig deeper you may just find that this is yet another falsehood that is being told.

What the data shows about Social Security going broke:

Each year the Social Security Board of Trustees (SSBT) releases a report on the economic health of the program which provides all the data and in 2022 the numbers told the exact same story:

Social Security is going broke.

In fact, the SSBT Report clearly shows that the operating expenses to run the Social Security program will increase by 5.42% annually while payroll tax revenue to pay for the benefits will only grow by 3.80% over the next 9 years.

Coupling this issue of the ever-increasing operating expenses is the realization, by Trustees, that the country’s fertility rate is projected to only be 1.99% going forward.

This 1.99% fertility rate indicates that as more and more people enroll into Social Security and stop contributing to the program there will be less and less people taking their place in the workforce to fund the system through their payroll taxes.

Over the long haul it appears that it is just a matter of time before the Social Security program does go bust as the country will not have enough people to fund the system (think why immigration is unchecked right now).

The problems contributing to the demise of Social Security keep stacking up too as there seems to be some other force that has been steering the program to insolvency which began back in the 1990’s.

What the data doesn’t show about Social Security going broke:

Furthering the problem of Social Security going broke is one key piece of data that unless you are looking at it directly you would miss it in its entirety:

The rate of return on the assets held in the Trust Fund is dropping on a consistent basis annually.

To put this problem into perspective in 2022 the Trust Fund was flush with cash as there was over $2.666 trillion in it. During the year, according to the SSBT Report, these assets generated a whopping $61.8 billion in interest. This just happens to be a rate of return of 2.30%.

And this low rate of return on investible assets in 2022 is projected to go even lower through at least 2026, consequentially the Trustees expect to eventually see an increase in the rate of return.

This is where a huge red flag should pop up.

Looking back to 1996, 27 years ago, the rate of return on assets held in Social Security’s Trust Fund never grew from the previous year, in fact every year for 27 years it dropped by an average of 0.17%.

Yes, you are reading that right – over the span of at least 27 years the rate of return on assets held in the Trust Fund decreased every year.

To highlight this somewhat impossible feat, unless you were trying, below is simple chart breaking down just a few years that show the consistent decrease in the rate of return on assets held in the Trust Fund:

| Year | Assets (Billions) | Interest Earned (billions) | Return |

| 1996 | $567.0 | $38.7 | 6.83% |

| 2001 | $1,212.5 | $72.9 | 6.01% |

| 2006 | $1,844.3 | $91.8 | 4.98% |

| 2011 | $2,524.1 | $106.5 | 4.22% |

| 2016 | $2,801.3 | $87.0 | 3.11% |

| 2022 | $2,666.6 | $61.4 | 2.30% |

The future projections, which are not much better, are as follows:

| Year | Assets (Billions) | Interest Earned (billions) | Return |

| 2023 | $2,517.4 | $54.2 | 2.15% |

| 2024 | $2,342.6 | $49.0 | 2.09% |

| 2025 | $2,132.9 | $44.6 | 2.09% |

| 2026 | $1,893.5 | $41.3 | 2.18% |

| 2027 | $1,611.0 | $37.8 | 2.35% |

| 2028 | $1,277.1 | $32.2 | 2.52% |

| 2029 | $888.2 | $24.8 | 2.79% |

| 2030 | $441.0 | $16.5 | 3.74% |

From the charts above you can see that even though the country was in the midst of the greatest bull market in the history of the Stock Market, the federal government got a lower and lower rate of return each and every year.

As things look for the Social Security program with less taxpayer revenue, greater operating expenses, a future where there will be more takers than providers and a management staff that can not properly manage the assets on the books it should go bust much sooner than later, but believe it or not, it still is not and will not go broke.

Why Social Security is not going and will not go broke:

The simplest answer as to why Social Security is not going and will not go broke is Medicare.

Over the years the federal government, through Congress, has enacted key pieces of legislation that tie the two programs together and ensure that Medicare will be the savior of Social Security

These regulations are:

Regulation #1: You must enroll into Medicare when eligible to receive your Social Security benefit.

By law, for you or anyone else to receive Social Security benefits you must be at least 62 years of age, have applied for benefits and you are fully insured in terms of health coverage.

- This means if you are retired and are 65 years of age or older you must have Medicare.

- Failure to enroll into Medicare results in the immediate forfeiture of all Social Security benefits unless you are insured under another qualified health plan.

Regulation #2: Medicare premiums for Parts B and D are based solely on your income and the more you have the more you are going to pay.

By law, through Medicare’s Income Related Monthly Adjustment Amount (IRMAA) if your modified adjusted gross income (MAGI) exceeds certain thresholds for a given year your Medicare Part B and D premiums will be increased.

- MAGI is everything on lines 2a and 11 of the 2022 IRS tax-form 1040.

Regulation #3: The bulk of your Medicare premiums and any IRMAA surcharges you receive are automatically deducted from any Social Security benefit you receive.

By law, if your Social Security benefit does not cover your Medicare costs you will receive a bill in the mail.

- Medicare premiums are projected to inflate by at least 6.00% over the next 8 years.

- The Social Security cost of living adjustment (COLA) is expected to inflate by 2.40% over the next 8 years.

- Do the math.

These Regulations can be downloaded here

The reality of Medicare and IRMAA:

According to the Medicare Board of Trustees (MBT) in 2023 there will be about 54.8 million people enrolled into Part B who will also be receiving Social Security benefits.

The Trustees are also projecting that out of these 54.8 million people in Part B that just over 5 million of them will be subject to IRMAA.

These 5 million people are expected to pay an extra $20 billion in IRMAA surcharges for the year while also paying over $108 billion in Part B premiums.

This is a total of over $129 billion which all comes directly out of the benefits that Social Security is obligated to pay.

Therefore, with Medicare premiums and IRMAA Social Security doesn’t have to pay out the total obligation as Part B premiums and IRMAA surcharges will reduce those benefits.

The better news for Social Security, but not for you:

By 2031 the numbers of Medicare enrollees is expected to increase as more people are expected to retire. This phenomenon of more people retiring will speed up the process of saving Social Security.

In 2031 there will be a projected 65 million people enrolled into Medicare Part B who are also receiving Social Security.

Of these 65 million people at least 13 million of them are projected to be subjected to IRMAA.

These 13 million people will pay an extra $63.8 billion in IRMAA surcharges while also paying $212.5 billion in Part B premiums.

At least $276 billion will be deducted automatically from Social Security benefits in 2031 which does not include any reduction in benefits from those who choose to pay for their Medicare Part D or Medicare Advantage premiums through Social Security.

Since Social Security will be paying out less and less in benefits annually it will be able to keep more of the assets in the Trust Fund that were earmarked to help offset the difference between its Income and Operating Expenses.

A breakdown of the Trustees intermediate projections that do not include Medicare and IRMAA:

| Year | Total Income | Operating Expenses | Difference |

| 2023 | $1,100,800,000,000 | $1,169,800,000,000 | -$69,000,000,000 |

| 2024 | $1,144,900,000,000 | $1,244,800,000,000 | -$99,900,000,000 |

| 2025 | $1,195,700,000,000 | $1,332,700,000,000 | -$137,000,000,000 |

| 2026 | $1,257,700,000,000 | $1,414,700,000,000 | -$157,000,000,000 |

| 2027 | $1,313,400,000,000 | $1,499,700,000,000 | -$186,300,000,000 |

| 2028 | $1,370,300,000,000 | $1,591,100,000,000 | -$220,800,000,000 |

| 2029 | $1,427,000,000,000 | $1,685,200,000,000 | -$258,200,000,000 |

| 2030 | $1,482,700,000,000 | $1,781,900,000,000 | -$299,200,000,000 |

| 2031 | $1,539,400,000,000 | $1,881,000,000,000 | -$341,600,000,000 |

The breakdown of the Trustees projections with IRMAA surcharges and Medicare Part B premiums:

| Year | Total Income (billions) | Operating Expenses (billions) | Total Medicare (Billions) | Difference (billions) | Interest Rate | Added to Income (billions) |

| 2023 | $1,101 | $1,169.8 | $129.1 | $60.1 | 2.15% | $61.4 |

| 2024 | $1,206 | $1,244.8 | $141.9 | $103.4 | 2.09% | $105.5 |

| 2025 | $1,301 | $1,332.7 | $167.3 | $135.8 | 2.09% | $138.7 |

| 2026 | $1,396 | $1,414.7 | $175.1 | $156.8 | 2.18% | $160.2 |

| 2027 | $1,474 | $1,499.7 | $195.1 | $169.1 | 2.35% | $173.1 |

| 2028 | $1,543 | $1,591.1 | $213.6 | $165.9 | 2.52% | $170.1 |

| 2029 | $1,597 | $1,685.2 | $233.9 | $145.9 | 2.79% | $149.9 |

| 2030 | $1,633 | $1,781.9 | $253.6 | $104.4 | 3.74% | $108.3 |

| 2031 | $1,648 | $1,881.0 | $276.2 | $43.0 |

So, is Social Security really going broke?

The answer, for at least the short term (2023 – 2031) is a resounding NO if you apply actual federal law into the equation.

Now, if those responsibilities of Social Security in terms of collecting Medicare premiums and IRMAA are neglected then the answer is of course YES, it is going broke and taxes need to be raised immediately.

But is Social Security going broke in the long term?

With the realization that IRMAA is going to save the Social Security program at least in the near term there is still the issue of the country’s dwindling fertility rate coupled with the growing rate of people reaching retirement.

It is just a matter of time when a disproportionate amount of people will be collecting Social Security benefits verses a much smaller amount of people paying taxes to fund the system. This would mean that yes, the Social Security program should go broke, but, again, thankfully, there is still IRMAA

To save Social Security over the long term all that needs to be done is:

- Increase Medicare premiums at a slightly higher rate of inflation than the projected 6.46% rate.

- Or lower the IRMAA Threshold to entrap even more people.

- Or increase the surcharges to make those in IRMAA lose more of their Social Security benefit.

- Or do all three every year going forward.

Given the past track record of the federal government when it comes to generating revenue off the backs of the U.S. taxpayer to keep a program viable it would appear that the 4th option is the one that will most likely be applied.

The key question you have to ask yourself:

“Have you planned for IRMAA yet?”

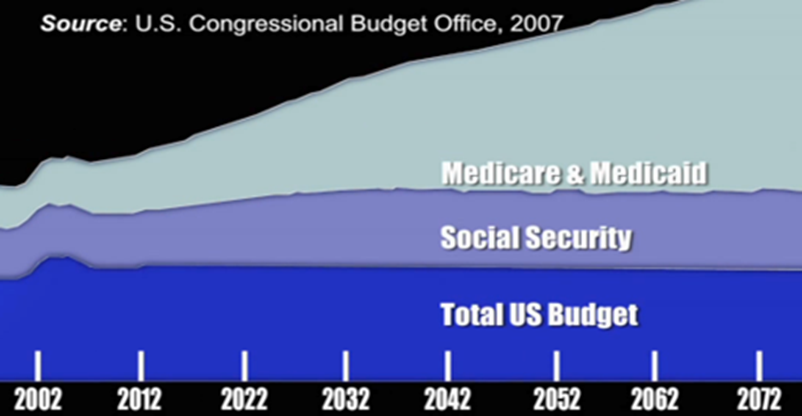

For those of you who still don’t believe that Social Security is not going broke:

Here is a chart from the Congressional Budget Office (CBO) that was published back in 2007 which ironically was the first year that IRMAA was implemented:

The above chart depicts how Medicare/Medicaid, Social Security and the overall Budget will perform through at least 2072.

As you can see as Medicare/Medicaid increases over time the Budget and Social Security remain steady.

The CBO knew back in 2007 that for Social Security and the Budget to remain steady all that was needed was for Medicare to increase in costs.

As people pay more for Part B premiums and IRMAA surcharge less will be paid out by Social Security while the federal government and the media can continue to convince you that your taxes must be raised to save all 3 of them.

It would appear the federal government is banking on you not planning for IRMAA!